Health insurance is one of those things everyone tells you to get, but few people explain simply. Most of us put it off, thinking we are young, or fit, or that the office already covers us. Then one unexpected hospital visit changes the maths.

In plain words, health insurance is a deal with an insurance company. You pay a fixed amount each year, and in return they cover your big hospital bills if you fall sick, get injured, or need surgery. Here is how to think about it, and whether you actually need one.

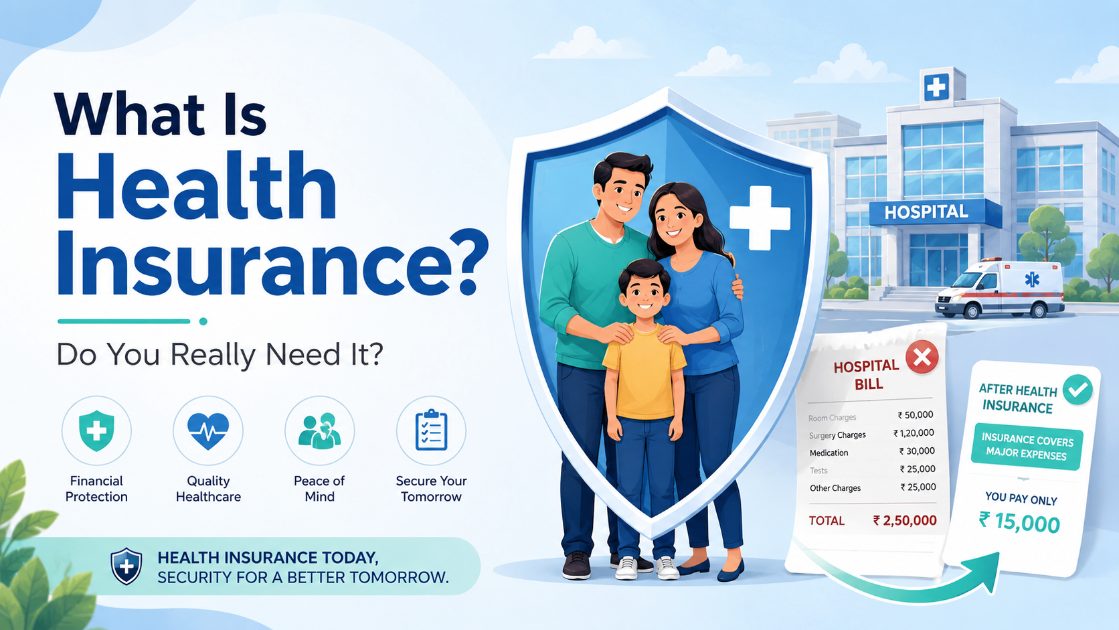

What is health insurance?

Health insurance is an agreement between you and an insurance company. You pay a fixed amount every year, called the premium. In return, the company pays your hospital bills if you fall sick, get injured, or need surgery. It does not cover a cold or a clinic visit. It covers the big, expensive things: hospitalisation, surgery, ICU care.

Why medical bills can wipe out your savings

Medical costs in India are rising fast. Healthcare inflation is running at around 13% a year, well above general price inflation. A heart surgery can cost Rs 3 to 5 lakh. A cancer treatment can cross Rs 10 to 15 lakh. A few days in a private hospital, with tests and medicines, can wipe out years of savings.

That is not a scare tactic. It is just what the bills look like.

Do you really need one?

For most people in India, yes. But the honest answer is not the same for everyone.

If your employer gives you group health insurance, that helps. But it is the company's policy, not yours. It ends on your last working day, whether you quit, get laid off, or switch jobs. And the sum insured, the maximum the insurer pays per year, is often small. Some employer plans cover just Rs 2 to 3 lakh, which is not enough for a serious condition.

If you are young and healthy, you might think you can wait a few years. Here is why buying early makes sense. Premiums are lower when you are young. A Rs 10 lakh cover for someone in their 20s costs around Rs 9,000 a year. The same cover in their 40s costs around Rs 15,000. Also, every policy has a waiting period, usually 2 to 3 years, before pre-existing conditions are covered. Buy now, and by the time you are older and more likely to need the policy, the waiting period is already done.

If you cannot afford a private policy at all, there is a government option. See the section below.

Key terms, in plain words

- Premium: what you pay every year to keep the policy active.

- Sum insured: the maximum the insurer will pay in a year. A Rs 5 lakh sum insured means the insurer covers up to Rs 5 lakh per year.

- Cashless: you go to a hospital in the insurer's network. The insurer pays the hospital directly. You do not pay upfront.

- Reimbursement: you pay the bill yourself, then claim the money back. This works at hospitals outside the network.

- Network hospital: a hospital the insurer has a formal tie-up with. Cashless claims only work at network hospitals.

- Waiting period: a time gap, typically 2 to 3 years, before certain conditions get covered. You cannot claim for those specific conditions during this time.

- Room rent limit: some policies cap how much they will pay for your hospital room per day. If you take a more expensive room than the cap, the insurer may reduce your entire bill proportionately, not just the room cost. This is a common hidden problem. Check for it before buying.

- Co-pay: some policies ask you to pay a fixed share of every claim. A 10% co-pay on a Rs 2 lakh bill means you pay Rs 20,000 and the insurer pays the rest.

What about Ayushman Bharat?

The government runs Ayushman Bharat PM-JAY, a free health scheme for families in the bottom 40% of the population. Eligible families get Rs 5 lakh of health cover per year for hospitalisation at government hospitals and many empanelled private ones. Eligibility is based on SECC 2011 data, roughly around 12 crore families. From September 2024, all senior citizens aged 70 and above became eligible regardless of income. Check if your family qualifies at pmjay.gov.in.

Three things worth watching out for

- Room rent caps: a policy that limits your daily room to Rs 3,000 sounds reasonable until you pick a room that costs more and the insurer cuts your whole bill proportionately. Look for policies without a room rent cap.

- Waiting periods: before buying, read the full list of conditions with waiting periods, especially if you already have something like diabetes or hypertension.

- Investment-plus-insurance plans: some agents will pitch plans that combine health cover, life cover, and investment returns in one product. These are complex and usually more expensive than you need. A plain health insurance policy does the job more cleanly.

A few myths, cleared up

- "I'm young, I don't need this yet." Accidents, infections, and appendicitis do not check your age. A hospital stay at 24 costs the same as it does at 54.

- "My company covers me, so I'm fine." That cover is the company's, not yours. The day your job ends, the cover ends.

- "Insurance is only for old or sick people." It is designed to work best when you buy it before you need it. That is the whole point of insurance.

Same illness, very different bill

Take two colleagues, Priya and Anil. Both are 35 and earning well. A few years ago Priya bought a Rs 10 lakh health cover for about Rs 12,000 a year. Anil kept meaning to, but never got around to it.

Last year both needed the same surgery, a bill of about Rs 4 lakh. Priya's insurer paid the hospital directly, and she walked out having paid almost nothing. Anil paid the full Rs 4 lakh from his savings, money he had been setting aside for his daughter's school.

Same age, same illness, same bill. The only difference was one small yearly payment, made in time.

Questions people often ask

What is the difference between health insurance and life insurance?

Health insurance pays your hospital bills when you are sick or injured. Life insurance pays your family a lump sum if you die. Both protect you, but against different things. You may need both at some point.

Can I get a policy if I already have a condition like diabetes?

Yes. Most insurers will still give you a policy. Your pre-existing condition will typically have a waiting period of 2 to 3 years before the insurer covers it. After that waiting period ends, it is included like any other condition.

How much cover is enough?

Most financial planners suggest at least Rs 5 to 10 lakh for an individual. If you live in a city with large private hospitals, lean toward the higher end. Medical costs keep rising, so a higher sum insured holds its value better over time.

Does health insurance cover doctor visits and medicines outside the hospital?

Standard policies cover hospitalisation, meaning you are admitted for more than 24 hours. OPD visits and outpatient medicines are usually a separate add-on. Read the policy carefully before assuming they are included.

If you help people choose a health plan

Choosing the right cover confuses most people, which is why insurance advisors and agents spend so much time on calls explaining the options. If that is your work, it helps to know a little about each person before you talk, their age, family size, any existing conditions, and what they are worried about.

SurveyHeart's Consultation Booking Form lets a client book a call and share those details in advance, all in one simple form you send by link. It is free, works on any device, and the person filling it does not need to log in or install anything. Use the Consultation Booking Form.

If you take away one thing

Health insurance is cheapest and easiest to get when you are young and healthy, which is exactly when you feel you need it least. A simple plan with a sum insured of at least Rs 5 to 10 lakh, bought early, means the cover is ready long before the day you need it.

You do not have to decide today. Just do not leave it for the day the bill arrives.

This is general information to help you understand health insurance. Before buying any plan, read the full policy document and speak to a licensed insurance advisor. Terms, exclusions, and premiums vary by insurer and plan.