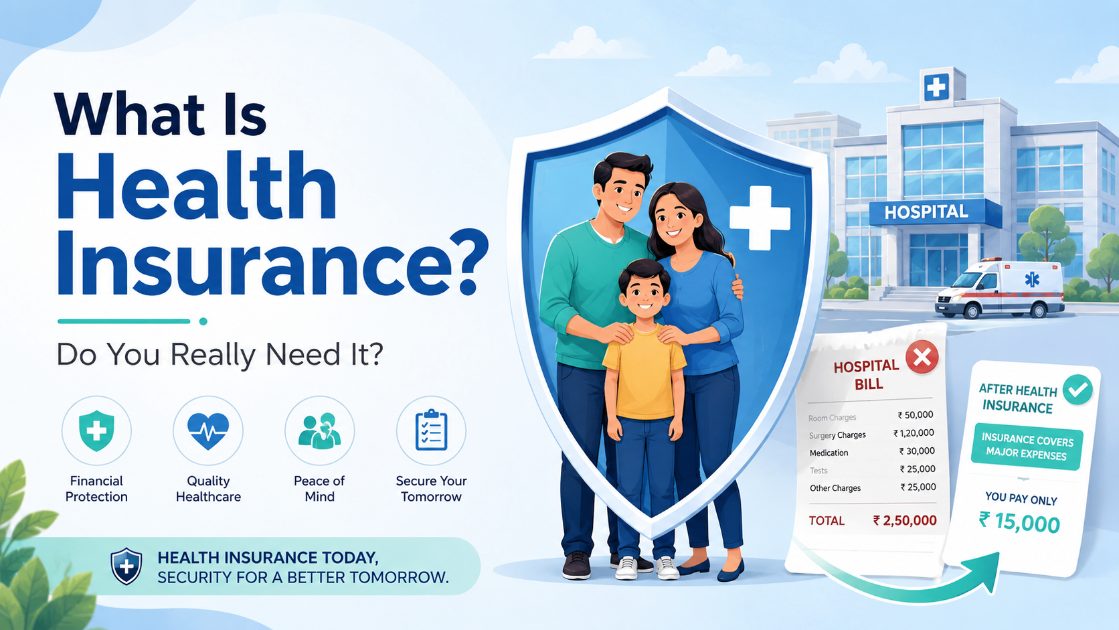

What is health insurance, and do you really need it?

You have probably heard the words health insurance many times. In ads, from a relative, or from a friend who just started a job. But what does it actually mean? Let us keep it very simple, as if you are hearing about it for the first time.

Think of it like a group safety net. Going to a hospital can cost a lot of money, and most people cannot keep that much aside for a sudden bill. So a large number of people each put in a small amount every year into one common pool. When any one of them ends up in hospital, that pool pays the big bill. You pay a little each year, and in return you are protected from a very large bill one day.

What is health insurance?

Health insurance is a simple deal between you and an insurance company. You pay them a small fixed amount once a year. This is called the premium. In return, if you fall sick and have to stay in a hospital, they pay the big bills. It is meant for the costly things, like an operation, an accident, or a few days of hospital care. It does not pay for a normal doctor visit or everyday medicines.

Why does it matter?

Hospital costs in India are high, and they go up every year, by around 13 percent. One big treatment can cost a few lakh rupees. A serious illness can cost much more. For most families, paying all of that suddenly from savings is very hard. Health insurance is simply a way to be ready for that day, so one hospital visit does not take away years of saving.

Do you really need one?

For most people, yes. But let us be honest, it depends a little on your situation.

If your office already gives you health insurance, that is good. But remember, that policy belongs to the company, not to you. The day you leave the job, it stops. And the amount it covers is often small, sometimes just two or three lakh, which may not be enough for a serious illness.

If you are young and healthy, you may feel there is no hurry. But starting early is cheaper and smarter. When you are young, the yearly premium is low. A ten lakh cover can cost around nine thousand rupees a year in your twenties, and more as you grow older. Also, every policy makes you wait two to three years before it covers an illness you already have. If you start early, that waiting time is already over by the time you really need it.

And if buying a policy is not possible for you right now, the government has a free option. More on that just below.

Some simple words you will hear

- Premium: the amount you pay every year to keep the policy active.

- Sum insured: the most the company will pay in a year. A five lakh sum insured means they cover your bills up to five lakh that year.

- Cashless: you go to a hospital that has a tie-up with your insurer, and the insurer pays the hospital directly. You do not pay from your own pocket.

- Network hospital: a hospital that has that tie-up with your insurer. Cashless only works at these hospitals.

- Reimbursement: you pay the bill first, and the insurer returns the money to you later.

- Waiting period: a gap of about two to three years before the policy covers an illness you already had when you bought it.

- Room rent limit: some policies set a cap on the room price they will pay per day. If you choose a costlier room, they may cut down your whole bill, not just the room part. It is good to check this before buying.

- Co-pay: some policies ask you to pay a small share of each bill yourself, and the insurer pays the rest.

What if you cannot afford a policy?

The government runs a free scheme called Ayushman Bharat PM-JAY. Families in the lower income group get up to five lakh rupees of free hospital cover every year, at government hospitals and many private ones too. It covers around twelve crore families, based on the 2011 survey list. From September 2024, every senior citizen aged seventy and above can join, whatever their income. You can check if your family is eligible at pmjay.gov.in.

A few things to check before you buy

- Room rent cap: try to pick a policy that does not put a limit on your room price, so your bill is not cut down later.

- Waiting periods: read which illnesses have a waiting time, especially if you already have something like diabetes or blood pressure.

- Mixed plans: some agents push plans that combine insurance with investment. These are usually costlier and harder to understand. A simple, plain health policy is enough for most people.

A few common myths

- "I am young, I do not need it yet." Accidents and sudden illness do not wait for age. A hospital stay costs the same at twenty four as it does at fifty four.

- "My company covers me, so I am fine." That cover belongs to the company. The day the job ends, the cover ends.

- "Insurance is only for old or sick people." It works best when you take it before you need it. That is the whole idea.

Common questions

What is the difference between health insurance and life insurance?

Health insurance pays your hospital bills when you are sick or hurt. Life insurance pays your family a fixed amount if you pass away. Both help you, but in different ways.

Can I get a policy if I already have something like diabetes?

Yes. Most insurers will still give you one. That illness usually has a waiting time of two to three years before it is covered. After that, it is covered like anything else.

How much cover is enough?

For one person, most advisors suggest at least five to ten lakh. If you live in a big city with costly hospitals, lean towards the higher side.

Does it pay for normal doctor visits and medicines?

Usually no. A normal policy covers hospital stays of more than twenty four hours. Doctor visits and daily medicines are a separate add-on. Always read what is included.

This is general information to help you understand health insurance in a simple way. Before buying any plan, read the full policy paper and talk to a licensed advisor. The exact terms and prices change from plan to plan.

SurveyHeart is a free form and survey tool used by over 10 million people in India. If you ever need to collect information, feedback, or responses of any kind, you can build and share a form in minutes. The people who fill it do not need to create an account.

Try it free at surveyheart.com.